Category: Payments and banks

Counterparty verification in CIS countries: Kazakhstan

We would like to draw your attention to the screening possibilities of foreign counterparties in the Republic of Kazakhstan.

To reduce risks and check the reliability, solvency and security of your foreign counterparty, you should take the following steps:

- Legal check;

- Financial check;

- Check valid licences, if applicable;

- Check other factors such as publicly available information / business reputation: customer reviews, relationships with partners or contractors.

As part of the legal review of an LLP (Limited Liability Partnership or “TOO”), which acts as a separate legal entity based on its own Charter, you should request the following legal documents:

- Charter;

- Memorandum of Association (however, the counterparty may refuse to provide this as the provisions may be confidential);

- Resolution/protocol on the appointment of the directors;

- State registration certificate – certificate of registration. What to check: Consistency of the information in the certificate with other incorporation documents;

- Business Identification Number (BIN) – a unique number created for a legal entity (branch and representative office) and self-employed persons;

- Registration number of the VAT payer’s certificate.

Also pay attention to the company’s legal address for local authorities. It must be specified in the Charter and other documents when registering the LLP and can be either a commercial premises or a private address (e.g. the founder’s flat).

There are following risk factors:

- “mass registration address”;

- mismatch between the legal and actual addresses (when submitting to the tax office), which is especially relevant for VAT payer counterparties.

The charter capital of an LLP must be at least 100 times the monthly calculate on index (MCI) at the time of submitting the formation documents for state registration. Fr om January 1, 2024, the MCI will be 3,692 tenge, i.e. the minimum capital must be 369,700 tenge (approx. RUB 73,000). The charter capital must be fully paid within one year from the date of registration. For small companies (up to 100 employees, income up to 300,000 MCI/year) there is no minimum capital (it can therefore be 0 tenge).

The executive body can be collective (directorate) or individual (director). An LLP can have several directors who act independently of each other (but only natural persons).

In addition, we would like to draw your attention to the official regime of “suspension of activity” in the Republic of Kazakhstan (the official analogue of “sleep mode” in the Russian Federation). During suspension, a company cannot conduct any profitable activities, but it is not liquidated and can be reinstated. Information on companies whose activities have been suspended can be obtained from the website of the State Revenue Committee of the Ministry of Finance of the Republic of Kazakhstan (SRC).

Further, in case the signatory of the contract is a director acting on the basis of the Charter, you should check the following aspects:

- Timeliness of the authorization (the data in the decision / protocol of appointment should coincide with the data in the state registers);

- Duration of the authorization;

- Existence of possible restrictions (e.g. transactions above a certain amount may require the approval of the participants, this may be specified in the Charter);

- Delimitation of powers if there are several directors.

If the signatory of the contract is acting on the basis of a power of attorney, be sure to request and scrutinize it for:

- The authority of the person issuing the power of attorney. If it is not signed by a director, but by another person based on the power of attorney with the right of overriding power of attorney, you should also request and check the original power of attorney;

- Description of the powers of the person acting on the basis of the power of attorney.

Wh ere to get data (open sources):

- Portal of the Bureau of National Statistics of the Agency for Strategic Planning and Reforms of the Republic Kazakhstan (RK).

Here you can find basic information about the company.

- Portal of the State Revenue Committee of the Ministry of Finance of the RK (www.kgd.gov.kz).

Here you can find:

- Details on suspension / non-suspension of activities;

- Information on the absence (presence) of tax arrears;

- Total amount of taxes paid;

- Presence of the counterparty in the List of unreliable taxpayers;

- Information about being / not being in the process of liquidation.

Here you can find the availability of open and past court cases.

- Public procurement portal.

Here you can see if the counterparty is on the list of unfair participants in public procurement.

- Portal of the Electronic Government of the Republic of Kazakhstan Egov.kz.

Here you can find:

- Information about the registered legal entity as of a given date;

- Details of the latest amendments to the constituent documents;

- Information about participation of the legal entity in other legal entities;

- Information on the presence of branches and representative offices of the legal entity;

- Information on the category of the subject of entrepreneurship;

- Data on encumbrances (seizure) on the legal entity’s share;

- Information on recognition of the legal entity as an inactive legal entity or involvement of its participants in inactive legal entities.

Unfortunately, as in many other jurisdictions, to obtain full data from public official sources, in most cases verification or authorization may be required, which requires a local phone number or IIN / BIN (analogue to the Russian TIN). In this regard, it may be necessary to engage a local partner to carry out a full-fledged verification.

For bigger or more significant deals, of course, the financial condition of the counterparty should be checked. For this purpose, it is necessary to request and analyze financial and tax statements for the last reporting periods:

- Balance sheet,

- Profit and Loss Statement,

- Cash flow statement.

Analyzing the financial statements will help to understand how successful and sustainable the company is, and to identify problems / risk factors.

We would also advise you to look at:

- review of financial ratios,

- analysis of current assets and total debt,

- profit and loss analysis,

- and get information about the bank details of the counterparty in advance – not all banks in Kazakhstan accept and send payments to Russia or do so with restrictions on the type of currency / banks from the Russian Federation.

We will be happy to answer your questions and, if necessary, carry out a counterparty check at your request.

Contacts:

Maria Matrossowa

Nadezhda Maskaeva

Other news

09.04.2026

March 26, 2026 – Winner in the “Legal Services” category at the annual Russian Business Guide. People of the Year Award

Review article “International payment practices in the current environment”

Exclusively for the Russian Business Guide magazine, Daria Pogodina, Managing Director of swilar presented a review article “International payment practices in the current environment”.

You can read the article online in Russian or English, or download two-language article in pdf-format by clicking the “Download en” button below the message.

Other news

09.04.2026

March 26, 2026 – Winner in the “Legal Services” category at the annual Russian Business Guide. People of the Year Award

CFO – Payments to friendly countries as of June 2024

Daria Pogodina presented an up-to-date overview of the regulation of cross-border settlements with so-called friendly jurisdictions, highlighted the requirements of currency legislation, the practice of banking support and the nuances of interaction with the government commission. The report was aimed at financial directors and aroused keen interest due to its practical focus and relevance.

Other news

09.04.2026

March 26, 2026 – Winner in the “Legal Services” category at the annual Russian Business Guide. People of the Year Award

“Russia – Turkey: from import-export to investment cooperation”

Daria Pogodina covered current mechanisms of cross-border settlements, features of interaction with Turkish counterparties, currency control requirements and banking practices. Particular attention was paid to opportunities for simplifying settlements and reducing associated risks. The article aroused interest among participants working in the field of foreign economic activity and investment.

Other news

09.04.2026

March 26, 2026 – Winner in the “Legal Services” category at the annual Russian Business Guide. People of the Year Award

French Chamber – situation with payments to friendly countries as of May 2024

Daria Pogodina spoke at the meeting organized by the French Chamber of Commerce and Industry. During her speech Daria covered the current rules for settlements with jurisdictions that are not subject to sanctions restrictions including the specifics of currency control, requirements for justifying payments and interaction with banks. The report was accompanied by practical recommendations and answers to questions from participants, which made it especially useful for companies with an international structure.

Other news

09.04.2026

March 26, 2026 – Winner in the “Legal Services” category at the annual Russian Business Guide. People of the Year Award

WG Accounting of AHK

During her speech, Yevgenia Chernova covered in detail the key changes in the rules of transfer pricing, which came into force at the beginning of 2024. Special attention was paid to the practical aspects of the application of new norms for companies operating in a special economic zone. The presentation aroused great interest and became a reason for discussion among the participants.

Other news

09.04.2026

March 26, 2026 – Winner in the “Legal Services” category at the annual Russian Business Guide. People of the Year Award

International payments and account opening difficulties

An increasing number of Russian banks are now suspending the opening of accounts for new customers, restricting the opening of new foreign currency accounts for existing customers, introducing commissions for keeping foreign currency in accounts, and imposing limits on foreign currency transfers or ceasing to make such transfers abroad altogether.

We continuously monitor the situation with local banks, keep track of updates on the conditions with foreign currency international transfers with European and CIS countries, and maintain a consolidated analytical register, including for banks in Russia that are in the TOP-100 of current Russian financial sector rankings.

We also provide additional comprehensive account opening support to our clients, namely:

- full communication with the bank;

- clarification of the requirements for the package of documents to be submitted for account opening;

- preparation and verification of the set of documents required for account opening/provision of information on the documents required for account opening;

- completion of all required applications and forms;

- control over the opening of bank accounts;

- preparation of the documents for granting access to the online bank and connecting authorized signatories and non-signatories to the online bank.

Should you have any difficulties with international payments, account opening or other related issues, we will be happy to provide you with more detailed information upon request and offer our support.

Contacts:

Maria Matrossowa

Yulia Belokon

Other news

09.04.2026

March 26, 2026 – Winner in the “Legal Services” category at the annual Russian Business Guide. People of the Year Award

FAQ – peculiarities of work with special C-type accounts

We would like to draw your attention to the recent clarifications issued by the Central Bank of Russia (hereinafter referred to as the “Central Bank”) regarding the relevant changes in legislation in accordance with the Presidential Decrees.

On 05.03.2022, Presidential Decree No. 95 “On the temporary procedure for meeting obligations to certain foreign creditors” (hereinafter referred to as Decree No. 95) was issued. Decree No. 737 of 15.09.2022 also introduces additional restrictions on payments to foreign residents – in particular, it concerns the implementation of payments to the participant in case of liquidation or reduction of shared capital (entered into force on 15.10.2022).

For which purposes it is compulsory to open a type C special account:

For payments in excess of 10 million rubles (or the equivalent in a foreign currency) per calendar month to “unfriendly” foreign counterparties, as well as to “friendly” foreign creditors, if the rights of claim on obligations passed to them fr om unfriendly foreign creditors after March 1, 2022 (Item 8 of Decree № 95) for:

- total liabilities of the debtor (including loan repayment and interest on it) on loans and borrowings, as well as payment of dividends/distribution of profits of Limited Liability Companies

- loans, borrowings, and financial instruments (including securities) of Joint Stock Companies

- fulfillment of obligations under concluded agreements which are derivative financial instruments

- purchase of real estate fr om “unfriendly” individuals

- Disbursement of funds by residents due to reduction of shared capital, liquidation or bankruptcy proceedings of resident legal entities (or permission obtained – Decree № 737 of 15.09.2022).

Who, where and in what currency should a type C account be opened:

- A resident sends an application to a credit institution in the name of a foreign creditor for a C-type account, whereby a bank account agreement does not need to be concluded.

A foreign creditor cannot open a C-type account on its own initiative (Letter of the Bank of Russia No. 019-12-4/2759 dated 06.04.2022).

- The C-type account is kept in rubles, is not opened in a foreign currency and cannot be opened in a foreign credit institution (clauses 3,5 of Decree No. 95).

- A bank account previously opened in the ordinary course of business will not be suitable for use as a C-type account, but depo accounts opened in the name of a foreign creditor before 24.03.2022 can be used.

When is a special account NOT needed?

- C-type accounts are not used if the aggregate amount of all debtor’s liabilities to all foreign creditors mentioned in Clause 1 of Decree No. 95 in a calendar month does not exceed 10 million rubles or its equivalent in foreign currency (at the official exchange rate of the Bank of Russia set as of the first day of the respective calendar month) or there is a permit from the Government Commission.

- If the obligation stipulated by Decree No. 95 is performed to a person who is not “unfriendly” (at the same time meeting the requirements set out in clause 12 of Decree No. 95 that the ultimate beneficiaries are the Russian Federation, its legal entities or individuals, and this information is disclosed to the tax authorities in an appropriate manner)

What is allowed when using a Type C account:

- It is possible to use a C-type account opened to a non-resident upon application of one resident for performance of obligations by other residents to the same non-resident and not to open a new C-type account.

- Transfer of funds to a non-resident to a C-type account opened with a bank different from the bank wh ere the resident is serviced.

- Transfer of rubles from a C-type account opened in favour of a non-resident legal entity of an “unfriendly” state in one credit institution to a C-type account of the same legal entity opened in another credit institution.

- There are no restrictions on residents using several C-type bank accounts for different obligations (contracts, products) in favour of one non-resident or applying one C-type account.

Limitations and specifics of the Type C account:

- Funds in the C-type account opened in the name of a foreign creditor belong to the foreign creditor from the moment the account is credited and until an agreement is concluded with the foreign creditor.

- The bank wh ere the C-type account was opened may not unilaterally close such account due to the absence of the foreign creditor’s application.

- A resident is not entitled to dispose of or request refund from a C-type bank account, except in case the funds were mistakenly credited to a C-type account.

- Transfer by the client from a C-type bank account to another non-resident bank account (opened both in the Russian Federation and abroad) is currently not possible (without authorisation).

For which purposes money can be written off:

- payment of taxes, duties, fees and other mandatory payments payable to the budget

- transfers for the purchase of federal loan bonds

- transfers to current accounts of non-residents in the currency of the Russian Federation, as stipulated by the permit

- transfers for other transactions provided for by the permit

- payment of commissions to the authorised bank servicing the account.

Contacts:

Eugenia Chernova

Olga Kireyeva

Other news

09.04.2026

March 26, 2026 – Winner in the “Legal Services” category at the annual Russian Business Guide. People of the Year Award

New standard FAS 14/2022 “Intangible Assets”

We would like to bring to your attention that the order of the Ministry of Finance dated 30 May 2022 N 86n approved the new standard FAS 14/2022 “INTANGIBLE ASSETS” (registered with the Ministry of Justice of Russia 28 June 2022, no. 69031).

The beginning date of application of the standard is the accounting period of 2024, with early application permitted.

Simultaneously with the adoption of the new standard, RAS 14/2007, “Accounting of intangible assets”, will be discontinued with effect fr om 1 January 2024.

Before adopting the new standard, we recommend the following actions:

- Conduct an inventory of the organisation’s intangible assets (hereinafter, IA) that could be classified as IA in accordance with FAS 14/2022;

- Establish a limit on the value of IA in order to classify acquisition and creation costs as IA, or recognise them as expenses for the period;

- Make changes to the company’s accounting policies;

- Determine the useful life expectancy of IA and the terms of annual useful life assessment for relevance;

- Choose the method of subsequent accounting of IA (after initial recognition), at initial or revalued cost (applicable if there is an active market for IA in accordance with IAS 38);

- Determine the residual value of IA on the company’s balance sheet and the terms of its annual valuation;

- For the method of valuation of IA at revalued cost, determine the frequency of revaluation for each group of IA;

- Reflect changes in the organisation’s balance sheet as at 01.01.2024 using incoming adjustments;

- Disclose information in the notes to the company’s accounting (financial) statements.

What does this mean in practice?

For accounting purposes, intangible assets are to be classified by type (electronic computer programmes (ECPs); databases; inventions; utility models; industrial designs; production secrets (know-how); selection achievements; licences and permits) and group.

The unit of accounting for intangible assets is an inventory item.

An inventory object of intangible assets is a set of rights to it arising in accordance with contracts or other documents confirming the existence of the organisation’s rights to such an asset.

A complex object that includes several protected results of intellectual activity (e.g., a multimedia product, a single technology) may also be recognised as an inventory object of intangible assets.

Under the new standard, an entity has the right to independently set a value lim it on the attribution of an item to either IA or expenditure for the period upon completion of capital expenditures related to the acquisition, creation of the assets (paragrath 7 FAS 14/2022).

The standard introduces the concept of residual value – the amount that an organisation would receive if the item were disposed of. The residual value of an IA is deemed to be zero, except in the following cases:

- a contract requires another party to purchase the intangible asset from the organisation at the end of its useful life;

- there is an active market for the item, from which its residual value can be determined;

- it is highly probable that an active market for the item will exist at the end of its useful life.

(paragraph 36 FAS 14/2022).

Depreciation elements such as the residual value, useful life and depreciation method should be reviewed systematically (at least at the end of each year) for changes and, if necessary, adjusted (paragraph 42 FAS 14/2022).

Transition period

Under paragraphs 52-54 of FAS 14/2022, the effects of a change in accounting policy arising from the adoption of the new standard should be recognised retrospectively – as if the standard had been applied from the start of the acquisition of IA.

However, an organisation has the option not to restate comparative amounts for periods prior to the reporting period, but to reflect the changes in carrying amounts resulting from the adoption of the standard through the organisation’s retained earnings.

Prospective application of the standard, without incoming adjustments at the beginning of the year is only possible for organisations that have the right to apply simplified accounting methods, including simplified (financial) reporting (paragraph 55 of FAS 14/2022).

Contacts:

Eugenia Chernova

Olga Kireyeva

Other news

09.04.2026

March 26, 2026 – Winner in the “Legal Services” category at the annual Russian Business Guide. People of the Year Award

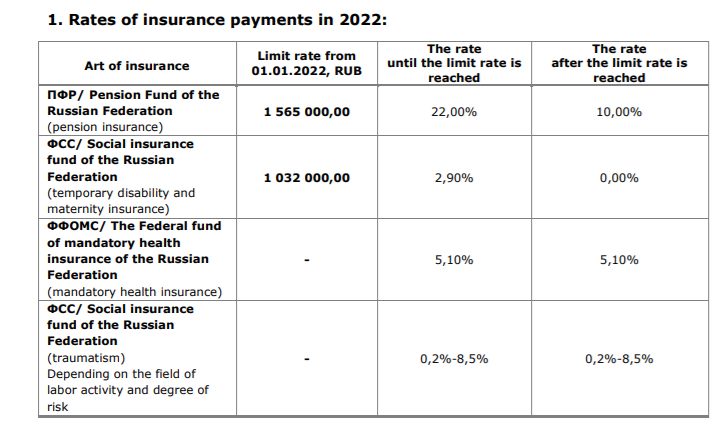

The rate limit for insurance payments in 2022

Оn January 1, 2022, the Resolution of the Government of the Russian Federation №1951 dd. 16.11.2021 comes into force. It concerns increasing the rate limit for insurance payments in cases of temporary disability and maternity, and also mandatory pension insurance:

- The rate limit for social insurance, in cases of temporary disability and maternity, for each individual does not exceed 1,032,000 rubles on a cumulative basis starting fr om the 1 January 2022;

- The rate limit for mandatory pension insurance does not exceed 1,565,000 rubles on a cumulative basis starting from the 1 January 2022 for each individual.

The payments for health care insurance and social payments in case of injuries will have to be made on the basis of all the taxable incomes irrespective of their amount. There will be no lim it for them, as before.

The limits and regulations for calculating insurance payments given above will be valid in 2022 for all companies, except for those with the status of SMEs.

2. Social contributions for SMEs in 2022:

We remind you that in accordance with the Federal Law of 01.04.2020 № 102-FZ dated April 1, 2020, the total amount of insurance payments for SME to state extrabudgetary funds in respect of payments to individuals, in excess of the minimum monthly wage, is reduced to 15%.

This reduced rate for SME applies irrespective of the maximum amount of payments to an individual (see above). At the same time, a part of payments less than or equal to the minimum monthly wage (determined at the end of each calendar month) is taxable at the general insurance contribution rate of 30%.

The value of the minimum monthly wage is set simultaneously on the entire territory of the Russian Federation by the federal law and is subject to annual indexation.

The minimum wage is established at the rate of 13 890 rubles for 2022 (Federal law N 406-FZ dated 06.12.2021).

Please note! Reduced tariff of insurance payments for SME from 01.01.2021 is determined for unlimited term (Item 17, clause 1, Art. 427 of the Tax Code, as amended from 01.01.2021).

We will be happy to answer your questions!

Contacts:

Natalia Safiulina

Ekaterina Babenko

Other news

09.04.2026