Category: Payments and banks

New standard FAS 14/2022 “Intangible Assets”

We would like to bring to your attention that the order of the Ministry of Finance dated 30 May 2022 N 86 approved the new standard FAS 14/2022 “INTANGIBLE ASSETS” (registered with the Ministry of Justice of Russia 28 June 2022, no. 69031).

The beginning date of application of the standard is the accounting period of 2024, with early application permitted.

Simultaneously with the adoption of the new standard, RAS 14/2007, “Accounting of intangible assets”, will be discontinued with effect fr om 1 January 2024.

Before adopting the new standard, we recommend the following actions:

- Conduct an inventory of the organisation’s intangible assets (hereinafter, IA) that could be classified as IA in accordance with FAS 14/2022;

- Establish a limit on the value of IA in order to classify acquisition and creation costs as IA, or recognise them as expenses for the period;

- Make changes to the company’s accounting policies;

- Determine the useful life expectancy of IA and the terms of annual useful life assessment for relevance;

- Choose the method of subsequent accounting of IA (after initial recognition), at initial or revalued cost (applicable if there is an active market for IA in accordance with IAS 38);

- Determine the residual value of IA on the company’s balance sheet and the terms of its annual valuation;

- For the method of valuation of IA at revalued cost, determine the frequency of revaluation for each group of IA;

- Reflect changes in the organisation’s balance sheet as at 01.01.2024 using incoming adjustments;

- Disclose information in the notes to the company’s accounting (financial) statements.

What does this mean in practice?

For accounting purposes, intangible assets are to be classified by type (electronic computer programmes (ECPs); databases; inventions; utility models; industrial designs; production secrets (know-how); selection achievements; licences and permits) and group.

The unit of accounting for intangible assets is an inventory item.

An inventory object of intangible assets is a set of rights to it arising in accordance with contracts or other documents confirming the existence of the organisation’s rights to such an asset.

A complex object that includes several protected results of intellectual activity (e.g., a multimedia product, a single technology) may also be recognised as an inventory object of intangible assets.

Under the new standard, an entity has the right to independently set a value lim it on the attribution of an item to either IA or expenditure for the period upon completion of capital expenditures related to the acquisition, creation of the assets (paragrath 7 FAS 14/2022).

The standard introduces the concept of residual value – the amount that an organisation would receive if the item were disposed of. The residual value of an IA is deemed to be zero, except in the following cases:

- a contract requires another party to purchase the intangible asset from the organisation at the end of its useful life;

- there is an active market for the item, from which its residual value can be determined;

- it is highly probable that an active market for the item will exist at the end of its useful life.

(paragraph 36 FAS 14/2022).

Depreciation elements such as the residual value, useful life and depreciation method should be reviewed systematically (at least at the end of each year) for changes and, if necessary, adjusted (paragraph 42 FAS 14/2022).

Transition period

Under paragraphs 52-54 of FAS 14/2022, the effects of a change in accounting policy arising from the adoption of the new standard should be recognised retrospectively – as if the standard had been applied from the start of the acquisition of IA.

However, an organisation has the option not to restate comparative amounts for periods prior to the reporting period, but to reflect the changes in carrying amounts resulting from the adoption of the standard through the organisation’s retained earnings.

Prospective application of the standard, without incoming adjustments at the beginning of the year is only possible for organisations that have the right to apply simplified accounting methods, including simplified (financial) reporting (paragraph 55 of FAS 14/2022).

Contacts:

Eugenia Chernova

Olga Kireyeva

Other news

04.08.2026

Overview of changes: Double Taxation Agreement (DTA) and deposits

28.07.2026

Amendments to the regulation of transactions with persons from unfriendly countries

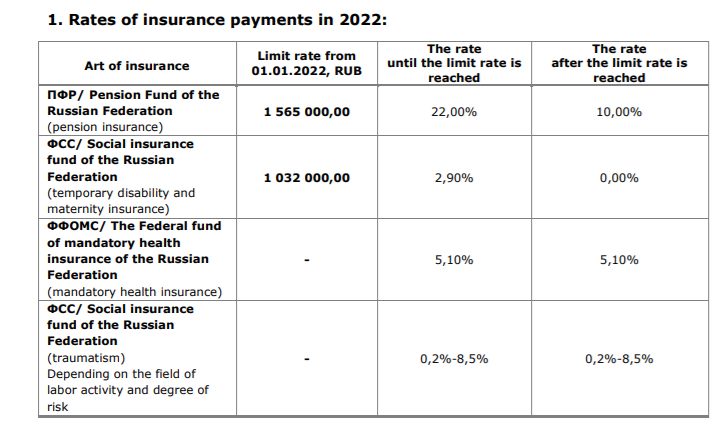

The rate limit for insurance payments in 2022

Оn January 1, 2022, the Resolution of the Government of the Russian Federation №1951 dd. 16.11.2021 comes into force. It concerns increasing the rate limit for insurance payments in cases of temporary disability and maternity, and also mandatory pension insurance:

- The rate limit for social insurance, in cases of temporary disability and maternity, for each individual does not exceed 1,032,000 rubles on a cumulative basis starting fr om the 1 January 2022;

- The rate limit for mandatory pension insurance does not exceed 1,565,000 rubles on a cumulative basis starting from the 1 January 2022 for each individual.

The payments for health care insurance and social payments in case of injuries will have to be made on the basis of all the taxable incomes irrespective of their amount. There will be no lim it for them, as before.

The limits and regulations for calculating insurance payments given above will be valid in 2022 for all companies, except for those with the status of SMEs.

2. Social contributions for SMEs in 2022:

We remind you that in accordance with the Federal Law of 01.04.2020 № 102-FZ dated April 1, 2020, the total amount of insurance payments for SME to state extrabudgetary funds in respect of payments to individuals, in excess of the minimum monthly wage, is reduced to 15%.

This reduced rate for SME applies irrespective of the maximum amount of payments to an individual (see above). At the same time, a part of payments less than or equal to the minimum monthly wage (determined at the end of each calendar month) is taxable at the general insurance contribution rate of 30%.

The value of the minimum monthly wage is set simultaneously on the entire territory of the Russian Federation by the federal law and is subject to annual indexation.

The minimum wage is established at the rate of 13 890 rubles for 2022 (Federal law N 406-FZ dated 06.12.2021).

Please note! Reduced tariff of insurance payments for SME from 01.01.2021 is determined for unlimited term (Item 17, clause 1, Art. 427 of the Tax Code, as amended from 01.01.2021).

We will be happy to answer your questions!

Contacts:

Natalia Safiulina

Ekaterina Babenko

Other news

04.08.2026

Overview of changes: Double Taxation Agreement (DTA) and deposits

28.07.2026

Amendments to the regulation of transactions with persons from unfriendly countries

Inclusion of license fees in the customs value

Earlier, we provided you with an overview of the current situation with the liquidation of LLCs in Russia.

In addition to the previous review, we would like to further draw your attention to this year’s innovation: a simplified liquidation procedure.

A simplified liquidation procedure is available for SMEs (for the latest information on the status of SMEs, see here and here) and allows you to reduce the time and cost of the liquidation procedure, as well as reduce possible risks of improper liquidation (for example, restrictions on participation and management in new companies within three years).

However, not all SMEs are eligible for simplified liquidation by default. To do this, the company must comply with a list of certain additional criteria.

What conditions must be met to be eligible for simplified liquidation?

- All founders (members) of the company made a resolution to terminate activities unanimously.

- The company is included in the unified register of small and medium enterprises (SMEs).

- The company is not a VAT payer (it is on a simplified tax system) or is exempt fr om VAT.

- The company does not have debts to creditors, including debts to employees and the state budget.

- There are no marks in the Unified State Register of Legal Entities about the inaccuracy of data and about the initiation of bankruptcy proceedings.

- The company has no real estate and vehicles in the property.

- The organization is not in the process of liquidation, reorganization or in the process of forced exclusion from the Unified State Register of Legal Entities by decision of the Federal Tax Service.

How to implement simplified liquidation?

To start a simplified liquidation, you must submit an application to the tax service on form P19001. At the moment, the paper and electronic formats of this form have not yet been approved, at the current stage, you can familiarize yourself with the draft form.

In the application, the founders (members) of the company confirm that:

- All financial obligations to counterparties have been fulfilled.

- All payments due to dismissed employees have been made.

- No later than one business day before exclusion from the Unified State Register of Legal Entities, all taxes have been paid and final tax reporting has been provided.

The application can be submitted electronically (using an enhanced qualified electronic signature of each participant), directly to the tax service on paper (notarization of signatures will be required) or through a notary public.

What is the time lim it for simplified liquidation?

The tax service will check the application and within 5 business days will make a decision on the upcoming exclusion of the company from the Unified State Register of Legal Entities or refusal.

In case of a positive decision by the tax service, information about the upcoming exclusion of the company from the register will be published in the Unified State Register of Legal Entities and in the State Registration Bulletin.

Within 3 months from the date of publication in the bulletin, the creditors of the company will be able to send their objections, if any.

If there are no objections from creditors within 3 months, the liquidated company will be excluded from the register.

It is important to know:

The initial conditions for simplified liquidation must be met at the time of exclusion. If during this period the company accumulates debts or assets, or fails to submit reports, simplified liquidation will not take place.

Contacts:

Maria Matrossowa

Project leader swilar OOO Project Manager of SWILAR LLC

maria.matrossowa@swilar.ru + 7 499 978 37 87 (ext. 308)Tatiana Ushakova

Other news

04.08.2026

Overview of changes: Double Taxation Agreement (DTA) and deposits

28.07.2026