Category: Payments and banks

Overview of changes: Double Taxation Agreement (DTA) and deposits

Dear Colleagues,

This review is related to two recent amendments in financial regulation affecting taxation and banking deposit operations for persons from unfriendly countries

1. Full suspension of the Double Taxation Agreement between Germany and Russia

Since January 1, 2027, the Agreement between the Russian Federation and the Federal Republic of Germany for the Avoidance of Double Taxation regarding to taxes on income and capital dated May 29, 1996, as well as the corresponding Protocol thereto, shall be fully terminated.

Background

The sphere of Double Taxation Agreements (DTAs) has been in a highly turbulent phase in recent years (see, for example, one of our previous reviews on this issue by the link).

The Ministry of Finance regularly updates the register of current DTAs and information on their status on its website. The latest update was published on July 14, 2026.

It should be reminded that Russia unilaterally suspended the application of certain provisions of several Double Taxation Agreements since August 8, 2023 (the Presidential Decree No. 585) – we reviewed this in more detail in the corresponding review.

The suspension affected certain provisions of the Agreement with Germany as well. In particular, the suspension by the Russian Federation covered provisions on the taxation of dividends, interest, royalties, income from real estate and salaries.

At the same time the Agreement itself, as a whole, has formally remained in effect until now.

However, on June 26, 2026, Germany notified the Russian Federation of the full suspension of the Agreement since January 1, 2027.

Key consequences

- Asymmetry of the situation. Germany is fully suspending the Agreement, while the list of norms suspended by Russia formally remains unchanged at the moment.

- Elimination of foreign tax credits. Taxpayers will no longer be able to credit taxes paid in one country against tax liabilities in the other. For individuals (tax residents of Russia) receiving income in Germany, double taxation may arise.

- Impact on business. German subsidiaries with Russian parent structures will no longer be able to benefit from reduced withholding tax rates on dividends, interest and royalties under the Agreement. The importance of proper transfer pricing documentation increases, as tax authorities will pay more attention to cross-border transactions.

Therefore, it should be reminded that since January 1, 2024 new stricter regulations have taken effect in Germany due to inclusion of Russia in the EU "blacklist" for tax purposes and the application of the German Tax Haven Defense Act (Steueroasen-Abwehrgesetz).

Accordingly, the full suspension of the DTA since 2027 further tightens and reinforces this situation. However, the German Federal Ministry of Finance uses the term "suspension" rather than "denunciation" in accordance with the Article 29 of the DTA. This means that the agreement is not formally terminated, but is merely temporarily not being applied.

2. Clarification of the procedure for bank deposits operations of foreign persons

The Presidential Decree No. 377 dated June 1, 2026, has expanded the list of obligations subject to the special procedure established by the Decree No. 95. It should be reminded that this refers to the mandatory permitting procedure for certain categories of payments (such as dividends, loans) where the amount exceeds the limit of 10 million rubles (or equivalent in foreign currency) per month. The specified payments require either permission from the Government Commission or should be made through the special type "C" accounts.

Since June 1, 2026, this procedure also applies to obligations of banks to repay deposits and pay interest to foreign creditors from unfriendly countries.

Key changes:

- Extension of the special procedure to bank deposits. Previously the Decree No. 95 regulated the procedure for fulfilling obligations to certain foreign creditors. As of June 1, 2026, obligations under bank deposits have been included in this list.

- Who is subject to this law: foreign companies from unfriendly countries (and structures controlled by them, with the exception of Russian legal entities), their branches and representative offices in the Russian Federation, as well as individuals who are the citizens of unfriendly countries.

- Who is not subject to this law: foreign citizens with a residence permit in Russia, as well as Russian companies whose participants/shareholders include persons from unfriendly countries.

On July 14, 2026, the Bank of Russia issued official clarifications that specify the implications of the Decree No. 377 for depositors. In particular, it was specified that:

- The threshold of 10 million rubles applies individually to each depositor and not to all foreign creditors of the bank in aggregate (which had previously given rise to a number of differing interpretations). Consequently, if obligations to a particular depositor in a calendar month do not exceed 10 million rubles, the special procedure under the Decree No. 95 does not apply.

- If the threshold of 10 million rubles is exceeded, the obligations are fulfilled by crediting funds to a type "C" account. The use of funds from such an account is only possible for permitted purposes or on the basis of a special permit from the Government Commission.

- The Decree applies exclusively to obligations under bank deposit agreements. Obligations under bank account agreements and correspondent account agreements do not fall within its scope.

- In case of early or scheduled repayment of a deposit, as well as interest payments, the special procedure applies. However, prior to the date for performance, the bank is not obliged to change the status of the deposit (e.g., convert it into a type "C" account). The extension of a deposit agreement is permitted; however, interest payments made upon renewal are subject to the requirements of the Decree No. 95.

We will be glad to answer your questions and help you understand the regulatory framework applicable to your specific issue.

Other news

28.07.2026

Amendments to the regulation of transactions with persons from unfriendly countries

29.06.2026

Swilar on the cover of the May issue of Russian Business Guide at the 29th St. Petersburg International Economic Forum

New review of the Supreme Court of the Russian Federation No. 8/2026: Risks in settlements and transactions with unfriendly foreign counterparties

Dear Colleagues,

On June 22, 2026, the Supreme Court of the Russian Federation has published important clarifications (Thematic review No. 8/2026 dated June 17, 2026), which significantly refine and change the approach to assessing risks in settlements and transactions with foreign counterparties from countries included in the list of states unfriendly to the Russian Federation.

The document establishes the trend of judicial practice toward recognizing as void any legal structures aimed at circumventing special economic measures.

The document summarizes the approaches of courts to mechanisms such as payment splitting, cession, conclusion of settlement agreements or direct transactions with assets.

Below we provide a brief summary of some conclusions of the Review, however, we highly recommend you to review the full text of the document.

1. Payment splitting: a new direction in judicial practice

The key conclusion of the paragraph 4 of the Review concerns payments to foreign counterparties from unfriendly states.

The Supreme Court of the Russian Federation specified that the formal division of payments ("artificial splitting" according the text of the document) on credit obligations into tranches of up to 10 million rubles with the aim of circumventing the special settlement procedure (Presidential Decree No. 95) constitutes an abuse of rights.

It should be reminded that under the Presidential Decree No. 95 of the Russian Federation dated March 5, 2022, the special procedure (including the mechanism of type "С" accounts) applies when the limit of 10 million rubles per month (or the according equivalent in other currency) is exceeded in respect of obligations to a specific foreign creditor.

Position of the Supreme Court of the Russian Federation: formal compliance with the monthly limit for each individual payment does not provide business immunity from scrutiny.

If the totality of transactions indicates an intention to circumvent the requirements of the Decree No. 95, such actions may be qualified as void on the basis of the Articles 10 and 168 of the Civil Code of the Russian Federation (abuse of rights).

Risk area:

Although the clarification of the Supreme Court of the Russian Federation concerns only loan agreements, it is important to consider that the restrictions initially introduced by the Decree No. 95 and applicable to them were subsequently extended by additional Decrees (with reference to the rules introduced by the Decree No. 95) and effectively also apply to other types of payments in favor of foreign persons (such as dividends, royalties and others).

In this regard, it can be expected that the new position of the court may be relevant not only for the situation described in the Review regarding credit obligations but also for other types of payments, such as:

- Intra-group financing and loans;

- License fees and royalties;

- Payment of dividends to foreign participants;

- Any other periodic transactions to the persons from unfriendly jurisdictions.

The following factors are now critical for risk assessment: the economic purpose of the transaction, the total amount of aggregate obligations, control under payment recipients by unfriendly jurisdictions and interconnection of all payments made.

2. Other significant conclusions summarized in the Review

In addition to the issue of payment splitting, the Supreme Court has summarized its position on several other important matters that shape a comprehensive risk landscape for businesses. Below are given the examples of some conclusions of the Review:

1) Real estate transactions controlled by persons from unfriendly states

Essence: a real estate purchase and sale agreement concluded by a Russian company controlled by a foreign person from an unfriendly jurisdiction (i.e., where such person holds a share of more than 50%) is void if no permission from the Government Commission has been obtained (subclause "a" of the Decree No. 81).

Conclusion: even in the absence of any fact of funds being transferred abroad, the fact of concluding a transaction in circumvention of the permitting procedure itself is qualified as a violation of public interests (clause 2 of the Article 168 of the Civil Code of the Russian Federation) and results in the transaction being recognized void.

2) Establishment of foreign control over strategic assets

Essence: transactions for the acquisition of shares (interests) in strategic enterprises (the Review refers to a port) without prior approval from the Government Commission (in accordance with the Law No. 57-FZ) are void.

Consequences: in addition to bilateral restitution, the recovery of shares in favor of the Russian Federation may be applied as a consequence (Part 11 of the Article 15 of Law No. 57-FZ).

3) Assignment of claims to a friendly state

Essence: the assignment of a claim under a contract whereby a foreign creditor from an unfriendly country assigns the claim to a Russian or other friendly counterparty solely for the purpose of receiving money in circumvention of type "C" or "O" accounts, is void (Articles 10 and 168 of the Civil Code of the Russian Federation).

This applies both to loans (Decree No. 95) and to license fees (Decree No. 322).

4) Settlement agreement

Essence: a settlement agreement that provides for the payment of money (e.g., compensation for intellectual property infringement) not directly to a foreign rights holder from an unfriendly country, but to its Russian representative (or other person) in circumvention of the permitting procedure (in the situation described in the Review – the transfer of funds to a special type "O" account), cannot be approved by the court and is void.

Conclusion: a settlement agreement is considered as a transaction to which the permitting procedure applies on the basis of the current restrictive measures, in accordance with the underlying logic of the situation. Should violations be identified, the agreement may be declared void on the basis of the Articles 10 and 168 of the Civil Code of the Russian Federation.

5) Limitation of liability of banks

Essence: Russian bank that has debited a client's funds and sent them through an intermediary bank in an unfriendly country shall not be liable for the losses of the client if the transfer was blocked by the intermediary due to sanctions imposed at a later date, which the bank did not know and could not have known at the time of the transfer.

Conclusion: the risk of the transfer being blocked by the intermediary bank in an unfriendly country lies with the client, provided that the Russian sending bank proves that it acted in good faith and could not have foreseen the imposition of restrictions.

Conclusions and recommendations

The extracts given above do not summarize all the conclusions covered in the Review. We recommend you to review the full text of the document.

To minimize risks, we recommend companies making settlements with foreign counterparties to pay attention to the following factors:

- Conduct an audit of current obligations to counterparties from unfriendly countries and verify the need to comply with restrictive measures and apply the special settlement procedure;

- Analyze the economic purpose of their transactions and identify any signs of artificial splitting;

- Assess aggregate obligations. When reviewing consider the aggregate volume of obligations to a foreign recipient from an unfriendly state, not only the amount of a single payment order;

- Review the ownership structure of foreign counterparties to identify possible factors of control by persons from unfriendly states;

Our team is ready to conduct a comprehensive analysis of your situation promptly and, if necessary, help to adjust the logic of your settlement arrangements in the light of the latest judicial practice developments.

Contacts:

Maria Matrossowa, Partner, Project Leader: maria.matrossowa@swilar.ru

Daria Pogodina, Partner: daria.pogodina@swilar.ru

Submit a request

Other news

28.07.2026

Amendments to the regulation of transactions with persons from unfriendly countries

Cryptocurrency as a payment method

Daria Pogodina wrote an article for the Russian-Turkish Dialogue Association which reviews current issues of doing business between Russia and Turkey. The article covers key aspects of economic relations, legal issues, as well as the specifics of interaction in the field of international payments and taxation. Particular attention is paid to strategic areas for developing cooperation and potential risks that companies face when entering the Turkish market.

Other news

29.06.2026

Swilar on the cover of the May issue of Russian Business Guide at the 29th St. Petersburg International Economic Forum

Situation with cross-border payments as of March 2025

Daria Pogodina presented a report on the topic “The situation with cross-border payments as of March 2025” in Lipetsk. During her speech Daria presented up-to-date information on the current state of cross-border settlements, including changes in the regulation of foreign exchange transactions and documentation requirements. Particular attention was paid to changes in international payment practices and the adaptation of businesses to new conditions. The report aroused interest among participants engaged in foreign economic activity.

Other news

29.06.2026

Swilar on the cover of the May issue of Russian Business Guide at the 29th St. Petersburg International Economic Forum

Topics 2025: Practical Experience and Recommendations for Business Operations in Changing Conditions

PROGRAM

1. Current situation with international payments — overview and practical recommendations. Cryptocurrency payments — new opportunities for business?

Daria Pogodina — Managing Partner, swilar

2. Possibilities of transfers within the framework of foreign economic activity in rubles and yua

Vasily Lukyanenko — Head of Department, JSC OTP Bank, Corporate Business Directorate

3. What to consider when working with personnel

Elena Balashova — Managing Partner, Balashova Legal Consultants

4. Liability insurance as an important element of risk management. Risks of directors and managers

Nikolay Artamonov — Underwriter for financial risks, JSC IC Turikum

5. Audit checklist — main errors identified by auditors in accounting and tax accounting based on the results of 2024 in the context of constant changes. Preparation for the annual audit

Olga Grigorieva – General Director of Sterngoff Audit LLC

6. Logistics and customs risks when importing to the Russian Federation. Latest practice: routes, customs control, inclusion of agent fees, dividends

Anna Dashicheva – Commercial Director of Polar Group LLC

Online seminar 13.12.2024: Doing Business in Russia – Practical Experience in New Circumstances

PROGRAM

Detailed reviews and Q&A session with experienced experts on the following topics

1. Doing business in Russia

Legal, tax, HR and migration issues. Basics.

2. Overview on bank transaction with Russia

SWIFT, currency exchange and other.

3. Practical experience of foreign companies in Russia

FAQ in the regular business processes.

International settlements in cryptocurrency in 2024. Recent changes and practice

Daria Pogodina spoke at the meeting of the Accounting Working Group of the Russian-German Chamber of Commerce with a report on the topic “International Settlements in Cryptocurrency in 2024. Recent Changes and Practice.” The speaker covered current changes in the regulation of cryptocurrency transactions, including new requirements for cross-border payments and legal aspects of using cryptocurrencies for international settlements. During the speech, recommendations were given for compliance with the law, and practical cases were considered demonstrating the successful use of cryptocurrencies in international business practice. The report aroused keen interest among accountants and specialists working with innovative financial instruments.

Other news

29.06.2026

Swilar on the cover of the May issue of Russian Business Guide at the 29th St. Petersburg International Economic Forum

An article on the legalization of the legal status of cryptocurrency: how will this help businesses?

Especially for the November RBG (Russian Business Guide) magazine, swilar CEO Daria Pogodina and swilar Controlling Department Specialist Natalia Samonova discussed the current topic of cryptocurrency.

Другие новости

29.06.2026

Swilar on the cover of the May issue of Russian Business Guide at the 29th St. Petersburg International Economic Forum

Account of a Russian LLC abroad

In the context of ongoing difficulties with international payments, many companies have found it necessary to open an account in a foreign bank.

However, it is important to remember that opening a bank account in another jurisdiction imposes a number of additional obligations on the company, including the submission of necessary reports and notifications.

In our review, we will look at how not to violate the law in this situation and how to avoid penalties.

Let’s take a step-by-step look at what a company has to do to comply correctly with all requirements.

1. Notify the Federal Tax Service of Russia.

It is necessary to notify the Federal Tax Service in the following cases:

- opening a bank account outside the Russian Federation;

- closing such an account;

- changing the account details.

All Russian organizations are required to submit the corresponding notification. (Part 2, Part 8 of Art. 12 of the Law No. 173-FZ). The notification should be sent to the tax authority at the location of the organization in the form approved by the Order of the Federal Tax Service of Russia dated 26.04.2024 N SD-7-14/349@, within one month from the date of opening (closing) an account or changing the details, respectively (Part 2 of Art. 12 of the Currency Control Law).

Two forms have been approved: one is for opening and closing an account (Appendix N1), the other is for changing the details of this account (Appendix N2).

The notification can be submitted to the tax authority on paper (in person, through a representative, by registered mail) or in electronic form via telecommunication channels (TCC) or through the taxpayer’s personal account (PA).

When making the first transfer to a bank account abroad, the organization needs to provide the Russian bank with a notificatio

on opening this account with a tax inspector’s note on its acceptance (Part 4 of Art. 12 of the Currency Control Law).

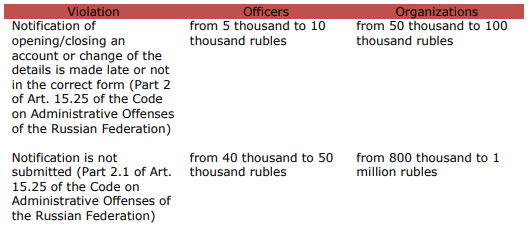

Failure to submit a notification about account or violation of the terms or procedure for submitting it may result in a penalty being imposed on the organization.

Their amounts are established in the Art. 15.25 of the Code on Administrative Offenses of the Russian Federation.

2. Report to the Federal Tax Service on flow of funds.

If a legal entity (resident of the Russian Federation) has foreign accounts, it has to submit a cash flow statement to the tax authority quarterly within 30 days after the end of the reporting quarter, attaching supporting documents: statements or other documents issued by the bank (Decree of the Government of the Russian Federation dated 28.12.2005 N 819 (as amended on 22.05.2024)).

If the documents are drawn up in a foreign language, the organization has to attach a translation into Russian, duly certified in accordance with the legislation of the Russian Federation (cl. 7 of the Rules for the Submission of Reports by Residents – Legal Entities).

The translation can be carried out by an employee of an organization or an organization engaged in translation activities, since the methods of translation are not limited by the law.

If necessary, at the request of the tax authorities, translation into Russian, notarized in accordance with the requirements of the legislation of the Russian Federation, shall be provided.

3. Comply with the currency legislation, in particular, carry out only legal currency transactions.

Contracts with non-residents, the amount of obligations for which exceeds the established threshold, namely, import contracts from 3 million rubles and export contracts from 10 million rubles, must be registered by an authorized bank of the Russian Federation.

The bank will assign a unique number to the contract (cl. 4.2, 5.5 of the Bank of Russia Instruction dated 16.08.2017 N 181-I (as amended on 09.01.2024).

When crediting export proceeds to an account abroad, it is necessary to provide to the authorized bank a certificate of currency transactions for settlements through an account abroad under accounting contracts, as well as provide a bank statement.

The term for providing a certificate of currency transactions for settlements through an account abroad is within 30 working days after the last day of the month in which such transactions were carried out.

4. Is it necessary to repatriate currency?

At present, the obligation to repatriate currency has only been retained for some companies.

From 16.10.2023 to 30.04.2025 inclusive, certain Russian exporters specified in the List approved by the Decree of the President of the Russian Federation dated 11.10.2023 No. 771, are required to credit to their accounts in authorized banks and sell proceeds in foreign currency on the domestic currency market of the Russian Federation within the established period and in the established amounts (cl. 1, 5 of the Decree of the Government of the Russian Federation dated 12.10.2023 No. 1681 “On measures for the implementation of the Decree of the President of the Russian Federation dated October 11, 2023 No. 771”).

The closed list consists of 43 groups of companies belonging to the sectors of the fuel and energy complex, ferrous and non-ferrous metallurgy, chemical and forestry industries, and grain farming. Exporters are notified of their inclusion in the list within 3 days by the Ministry of Economic Development of Russia.

For companies that are not on the closed list, the amount of foreign currency earnings subject to mandatory sale is currently 0%.

Therefore, if the organization is subject to the cancellation of repatriation, the terms for transferring export proceeds from the organization’s account opened abroad to a Russian bank are not established by regulation, i.e. such funds may remain on account abroad and these funds can be used, for example, for settlement of import or other contracts.

Contacts:

Natalia Safiulina

Nadezhda Kolomnikova

Other news

04.08.2026

Overview of changes: Double Taxation Agreement (DTA) and deposits

28.07.2026

Amendments to the regulation of transactions with persons from unfriendly countries

Online seminar 11/12/2024: Features of liquidation of companies with foreign participation: latest changes and practice

PROGRAM

1. Features of liquidation of foreign subsidiaries in 2024-2025.

Daria Pogodina, Managing Partner of swilar

2. Liquidation audit – features of the procedure.

Olga Grigorieva, General Director of Sterngoff Audit

3. Closing representative offices and branches of foreign companies – what to consider?

Daria Pogodina, Managing Partner of swilar

4. Features of termination of employment relations with employees during company liquidation.

Elena Balashova, Managing Partner of Balashova Legal Consultants

5. Planning the budget and financing of the company during the liquidation period.

Natalia Samonova, Head of Controlling Projects of swilar

6. Business valuation in Russia for the purpose of submission to the Government Commission.

Alexey Sitnikov, Director, Swiss Appraisal