Category: News

Information on participants of a foreign organization for 2024 – submit before 03/28/2025

Dear Clients,

please pay attention that the term for submission of information on the participants of a foreign organization for 2024 expires on March 28th, 2025.

All foreign organizations and foreign structures without formation of a legal entity registered with tax authorities in the Russian Federation are obliged to inform the tax authorities of all direct participants and beneficiaries regardless of the share of participation, as well as of indirect participation of an individual or a public company (if their share exceeds 5%).

The above-mentioned information is to be submitted to the tax authority not later than on March 28th each year. An exception is foreign organizations that are registered with a Russian tax authority only for provision of services in electronic form.

Non-submission or late submission of the information entails a fine of RUB 50,000.

You can find our earlier publications on this issue here and here.

We will gladly support you in preparing and submitting information on the participants/beneficiaries of a foreign organization to the tax authorities.

Other news

10.03.2026

Submission of information on participants of a foreign organization for 2025

Сhanges to corporate legislation: holding of meetings in companies

Dear Sirs or Mesdames,

we would like to inform you about the changes in the field of corporate law which will be important in the nearest time.

From March 01, 2025, significant new developments made by the Federal Law dated August 08, 2024 No. 287-FZ will come into force. A number of changes relates to limited liability companies (LLC).

So, the rules of holding general meetings of LLC participants have been amended, the related terminology has been changed. New rules will be applied, namely, while holding the annual meetings of participants according to the results of the year 2024.

Main changes are as follows:

The expression “general meeting” has been changed to “adoption of a resolution by the general meeting” or “meeting or absentee voting for adoption of a resolution by the general meeting”.

The meeting chairman will be elected only if the company does not have a Board of Directors (Supervisory Board). If it exists, the Chairman of such Board of Directors will take chair.

The forms of the general meeting will be as follows:

- a meeting, possible with remote participation;

- absentee voting, incl. by e-bulletins;

- a meeting combined with absentee voting.

In case of remote participation:

- participation will be executed using electronic/technical communications;

- a possibility is established to attend a meeting at the place of its holding or to hold a meeting without determining a place of holding;

- a possibility is established to make an online-broadcasting with access for the registered persons (upon a participant’s demand the company is obliged to provide access to the broadcasting recording).

Additionally, the rules of holding meetings combined with absentee voting have been fixed. Such meetings may be held in the cases stipulated by the company’s articles of association or by a unanimous resolution of all the company participants. Approval of annual reports and accounting (financial) statements is admitted at such meetings.

A separate article has been introduced dedicated to drafting and contents of the minutes of an LLC general meeting. It also stipulates that signing of the minutes by the secretary of the meeting will not be required.

Furthermore, a procedure was established in relation to adopting resolutions by the Board of Directors (the supervisory authority which is formed when it is stipulated by the articles of association). This authority may adopt resolutions at meetings (including those with remote participation) or by means of absentee voting. Similarly to meetings of company’s participants, meetings of the Board of Directors will be held with the possibility of personal attendance at the place of their holding as well as without determining such place.

The quorum when adopting Board resolutions will be not less than 1/2 of the number of Board members (if the greater number is not stipulated by the articles of association). The meeting may be combined with absentee voting.

The minutes according to the results of the meeting or the absentee voting will be prepared not later than 3 calendar days after the meeting or the end of document acceptance from the Board members (in case of absentee voting).

We will be happy to answer your questions arising in connection with the specified changes.

Your contacts on this topic:

Maria Matrosova

Nadezhda Maskaeva

Other news

10.03.2026

Submission of information on participants of a foreign organization for 2025

SWISS & RUSSIAN VIEWS AND PERSPECTIVES BY ACADEMIA AND BUSINESS

Daria Pogodina spoke at the conference “Swiss & Russian Views and Perspectives by Academia and Business” with the report on the topic “Practical Experience in Intercultural Communication with German-Speaking Countries”. As a part of the presentation, the speaker shared practical observations and cases from professional interaction with partners from Germany, Austria and Switzerland. The issues of differences in business culture, communication models were considered, and recommendations were given on how to build cooperation in an intercultural environment effectively. The report aroused keen interest among participants from the academic and business environment.

Review of FSBU 4/2023 “Accounting (financial) statements”

Elena Kameneva spoke at the meeting of the Accounting Working Group of the Russian-German Chamber of Commerce with a report on the topic “Review of FSBU 4/2023 “Accounting (financial) statements””. During the speech Elena analyzed in detail the main provisions of the new standard, which came into force in 2023 and its impact on the procedure for preparing and submitting financial statements. The report included an analysis of key changes, features of the standard’s application for Russian companies, as well as practical recommendations for implementing the new approach in accounting practice. The seminar aroused interest among specialists in the field of accounting and finance.

International settlements in cryptocurrency in 2024. Recent changes and practice

Daria Pogodina spoke at the meeting of the Accounting Working Group of the Russian-German Chamber of Commerce with a report on the topic “International Settlements in Cryptocurrency in 2024. Recent Changes and Practice.” The speaker covered current changes in the regulation of cryptocurrency transactions, including new requirements for cross-border payments and legal aspects of using cryptocurrencies for international settlements. During the speech, recommendations were given for compliance with the law, and practical cases were considered demonstrating the successful use of cryptocurrencies in international business practice. The report aroused keen interest among accountants and specialists working with innovative financial instruments.

An article on the legalization of the legal status of cryptocurrency: how will this help businesses?

Especially for the November RBG (Russian Business Guide) magazine, swilar CEO Daria Pogodina and swilar Controlling Department Specialist Natalia Samonova discussed the current topic of cryptocurrency.

Account of a Russian LLC abroad

In the context of ongoing difficulties with international payments, many companies have found it necessary to open an account in a foreign bank.

However, it is important to remember that opening a bank account in another jurisdiction imposes a number of additional obligations on the company, including the submission of necessary reports and notifications.

In our review, we will look at how not to violate the law in this situation and how to avoid penalties.

Let’s take a step-by-step look at what a company has to do to comply correctly with all requirements.

1. Notify the Federal Tax Service of Russia.

It is necessary to notify the Federal Tax Service in the following cases:

- opening a bank account outside the Russian Federation;

- closing such an account;

- changing the account details.

All Russian organizations are required to submit the corresponding notification. (Part 2, Part 8 of Art. 12 of the Law No. 173-FZ). The notification should be sent to the tax authority at the location of the organization in the form approved by the Order of the Federal Tax Service of Russia dated 26.04.2024 N SD-7-14/349@, within one month from the date of opening (closing) an account or changing the details, respectively (Part 2 of Art. 12 of the Currency Control Law).

Two forms have been approved: one is for opening and closing an account (Appendix N1), the other is for changing the details of this account (Appendix N2).

The notification can be submitted to the tax authority on paper (in person, through a representative, by registered mail) or in electronic form via telecommunication channels (TCC) or through the taxpayer’s personal account (PA).

When making the first transfer to a bank account abroad, the organization needs to provide the Russian bank with a notification on opening this account with a tax inspector’s note on its acceptance (Part 4 of Art. 12 of the Currency Control Law).

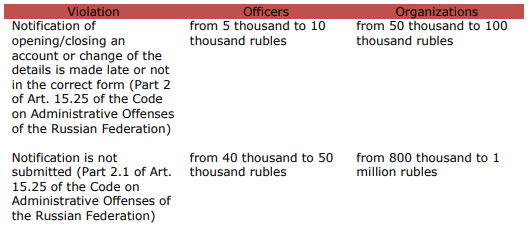

Failure to submit a notification about account or violation of the terms or procedure for submitting it may result in a penalty being imposed on the organization.

Their amounts are established in the Art. 15.25 of the Code on Administrative Offenses of the Russian Federation.

2. Report to the Federal Tax Service on flow of funds.

If a legal entity (resident of the Russian Federation) has foreign accounts, it has to submit a cash flow statement to the tax authority quarterly within 30 days after the end of the reporting quarter, attaching supporting documents: statements or other documents issued by the bank (Decree of the Government of the Russian Federation dated 28.12.2005 N 819 (as amended on 22.05.2024)).

If the documents are drawn up in a foreign language, the organization has to attach a translation into Russian, duly certified in accordance with the legislation of the Russian Federation (cl. 7 of the Rules for the Submission of Reports by Residents – Legal Entities).

The translation can be carried out by an employee of an organization or an organization engaged in translation activities, since the methods of translation are not limited by the law.

If necessary, at the request of the tax authorities, translation into Russian, notarized in accordance with the requirements of the legislation of the Russian Federation, shall be provided.

3. Comply with the currency legislation, in particular, carry out only legal currency transactions.

Contracts with non-residents, the amount of obligations for which exceeds the established threshold, namely, import contracts from 3 million rubles and export contracts from 10 million rubles, must be registered by an authorized bank of the Russian Federation.

The bank will assign a unique number to the contract (cl. 4.2, 5.5 of the Bank of Russia Instruction dated 16.08.2017 N 181-I (as amended on 09.01.2024).

When crediting export proceeds to an account abroad, it is necessary to provide to the authorized bank a certificate of currency transactions for settlements through an account abroad under accounting contracts, as well as provide a bank statement.

The term for providing a certificate of currency transactions for settlements through an account abroad is within 30 working days after the last day of the month in which such transactions were carried out.

4. Is it necessary to repatriate currency?

At present, the obligation to repatriate currency has only been retained for some companies.

From 16.10.2023 to 30.04.2025 inclusive, certain Russian exporters specified in the List approved by the Decree of the President of the Russian Federation dated 11.10.2023 No. 771, are required to credit to their accounts in authorized banks and sell proceeds in foreign currency on the domestic currency market of the Russian Federation within the established period and in the established amounts (cl. 1, 5 of the Decree of the Government of the Russian Federation dated 12.10.2023 No. 1681 “On measures for the implementation of the Decree of the President of the Russian Federation dated October 11, 2023 No. 771”).

The closed list consists of 43 groups of companies belonging to the sectors of the fuel and energy complex, ferrous and non-ferrous metallurgy, chemical and forestry industries, and grain farming. Exporters are notified of their inclusion in the list within 3 days by the Ministry of Economic Development of Russia.

For companies that are not on the closed list, the amount of foreign currency earnings subject to mandatory sale is currently 0%.

Therefore, if the organization is subject to the cancellation of repatriation, the terms for transferring export proceeds from the organization’s account opened abroad to a Russian bank are not established by regulation, i.e. such funds may remain on account abroad and these funds can be used, for example, for settlement of import or other contracts.

Contacts:

Natalia Safiulina

Nadezhda Kolomnikova

Other news

10.03.2026

Submission of information on participants of a foreign organization for 2025

Changes in regulating transactions with persons from unfriendly countries

At this moment, for companies with Western participation, coordination of transactions with the subcommittee of the Government Commission for Control of Foreign Investments in the Russian Federation remains of great relevance. The subcommittee has the right to make decisions on the issuance by the Government Commission of permits for residents of the Russian Federation to carry out transactions with foreign persons from unfriendly countries, as well as currency transactions.

We would like to remind you that unfriendly countries, in accordance with the order of the Government of the Russian Federation dated 05.03.2022 No. 430-р, include, among others, Australia, Great Britain, Canada, the Republic of Korea, the USA, Ukraine, Switzerland, Japan and all member states of the European Union.

In particular, in the Decree of the President of the Russian Federation dated 08.09.2022 No. 618 restrictions were established for the execution of transactions that directly and/or indirectly entail the establishment, change or termination of the rights of ownership, use and/or disposal of shares in the authorized capital of limited liability companies or other rights that make it possible to determine the conditions for management of such companies. First of all, these are transactions for disposal of shares in the authorized capital of limited liability companies, which have become relevant due to the desire of a number of Western companies to temporarily or permanently leave the Russian market due to the political situation.

Such transactions can only be carried out on the basis of permits issued by the Government Commission for Control of Foreign Investments in the Russian Federation, which, if necessary, contain the conditions for carrying out these transactions. The procedure and criteria for issuing permits are constantly updated with a tendency to become stricter, which is aimed at complicating the exit of Western businesses from the Russian market and maintaining their presence in the Russian Federation.

In addition to the requirements for documents that must be drawn up and submitted for approval, from the end of 2022, in order to alienate the share of an “unfriendly” participant of a limited liability company, it is necessary to pay a voluntary contribution to the budget of the Russian Federation (see our previous review on changes in this area), as well as to carry out the transaction with a mandatory discount.

At the end of October 2024, the Ministry of Finance of Russia published an updated regulation (Extract from the minutes of the meeting of the subcommittee of the Government Commission for Control of Foreign Investments in the Russian Federation dated 15.10.2024 No. 268/1). The new procedure includes the following:

- The amount of the voluntary contribution to be paid to the budget when Russian companies are disposed of by “unfriendly” participants has increased. Now it is 35% of the market value of the asset based on the results of its independent assessment (previously it was necessary to pay 15%).

An installment plan was introduced for payment of the contribution. 25% of the asset value must now be transferred to the Russian Federation budget within a month from the date of the transaction, 5% within a year, and another 5% within two years from that date. - In addition, the size of the mandatory discount to the market value of the asset upon alienation of an LLC has been changed. Now it must be a minimum of 60%, whereas previously the company could be sold for 50% of its market value.

Also, if the market value of the alienated assets is more than 50 billion rubles, the consent of the President of the Russian Federation will be required to complete the transaction.

The new conditions should apply both to future applications for approval of transactions, and to those already submitted, but not considered by the Government Commission.

Other news includes amendments to the Decree of the President of the Russian Federation dated 04.05.2022 No. 254 regarding the payment of profit of Russian resident companies to their foreign participants.

Let us remind you that in order to pay “unfriendly” participants profit in an amount exceeding 10 million rubles per calendar month or the equivalent of this amount in foreign currency, it is necessary to follow the procedure established by the Decree of the President of the Russian Federation dated 05.03.2022 No. 95. This procedure involves opening a special account of type “C” in a Russian credit institution in the name of a foreign creditor, through which the corresponding settlements are made. At the same time, the Ministry of Finance of the Russian Federation was given the authority to determine a different procedure for payment of residents’ profits to foreign creditors, which meant the need to obtain permissions from the Ministry of Finance for this procedure.

From 09.09.2024, the authority to issue permits for the payment of dividends by Russian companies to persons from unfriendly countries was granted to the Government Commission for Control of Foreign Investments in the Russian Federation. Such permits may contain conditions for the payment of profits.

The Government of the Russian Federation will additionally develop and approve the procedure for issuing such permits by the Government Commission. After the adoption of the changes, the procedure and terms for approving the payment of dividends may become milder.

We will keep you updated on the news of the relevant regulation, and are also ready to provide legal support when interacting with authorized bodies on issues of approving transactions and paying dividends to “unfriendly” foreign persons.

Other news

10.03.2026

Submission of information on participants of a foreign organization for 2025

Association Russian-Turkish Dialogue. Legalization of the legal status of cryptocurrency

The article by Daria Pogodina examines current changes in the legislation of Russia and Turkey concerning cryptocurrencies, as well as the process of their legalization and integration into the financial system of both countries. The author analyzes legal and regulatory barriers, and provides recommendations for businesses interested in using cryptocurrencies in their activities. The article focuses on the possible risks and benefits of using cryptocurrencies in international settlements.

They spoke at a meeting organized by the French Chamber of Commerce and Industry

Darya Pogodina spoke at an event organized by the French Chamber of Commerce and Industry with a report on the topic of “Counterparty verification in the CIS countries: Kazakhstan”. The speaker talked about the specifics of legal verification of partners in Kazakhstan, available sources of information, risks when concluding contracts and the specifics of corporate regulation. Participants received practical recommendations on reducing risks when entering the market and doing business with Kazakhstani companies.